Discover effective tips for creating a budget after getting your first job to secure your financial future today!

Starting your first job is exciting, but it can also be overwhelming. You suddenly have money coming in, and the temptation to spend is everywhere. But what if I told you that creating a budget after getting your first job can change everything? A budget is your roadmap to financial success. It helps you track where your money goes and allows you to save for the future.

Financial planning is essential, especially when you’re new to earning. You want to ensure that your hard-earned money is working for you. By understanding how to create a budget, you’ll not only avoid debt but also build a solid foundation for your financial future. Don’t worry; it’s easier than it sounds, and I’m here to guide you every step of the way.

To protect your income, consider insurance. It’s important to have a safety net in case life throws you a curveball. Learn more about how to protect your income with insurance.

In This Post, You’ll Learn:

- How to create a realistic budget you can stick to

- Where your hidden spending leaks are

- Tools that make money management easy

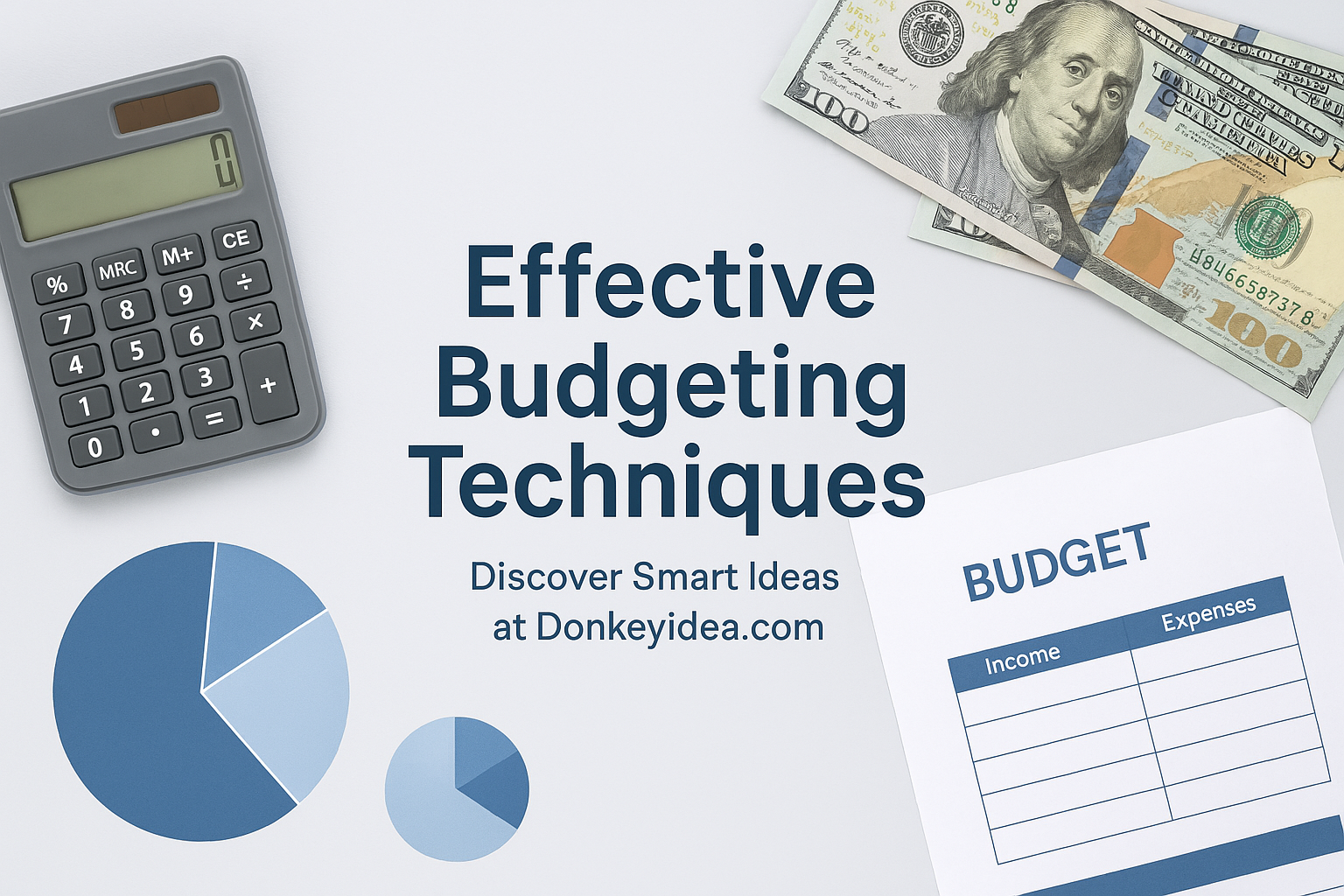

Create a Zero-Based Budget

What it is: A zero-based budget means every dollar you earn has a job. Your income minus your expenses equals zero.

Why it works: It forces you to think about your spending and makes sure you are not overspending.

How to do it: Write down your income and expenses. Adjust your budget until your total is zero.

Pro Tip: Use budgeting apps to keep track of your expenses easily.

Automate Your Savings

Why this helps: Automating your savings ensures you save money before you spend it.

How to set it up: Set up an automatic transfer from your checking account to your savings account each month.

Track Your Spending

What it is: Keeping track of every dollar you spend.

Why it matters: You’ll see where your money is going, and you can cut unnecessary expenses.

How to apply it: Use apps or a simple notebook to record your daily spending.

Pro Tip: Review your spending weekly to identify patterns and adjust your budget.

Set Financial Goals

What it is: Goals can be short-term (like buying new shoes) or long-term (like saving for a car).

Why it matters: Having clear goals keeps you motivated to stick to your budget.

How to apply it: Write down your goals and attach a timeline to them.

Pro Tip: Celebrate small milestones to keep yourself motivated.

Avoid Lifestyle Inflation

What it is: Spending more as you earn more.

Why it matters: This can lead to living paycheck to paycheck.

How to avoid it: Keep your lifestyle the same as when you were earning less.

Pro Tip: Use any extra income to boost your savings instead of spending it.

We also need to talk about the best life insurance plans for financial security. Life insurance can provide peace of mind and financial protection for your loved ones.

When I started tracking every expense, I realized I was spending way too much on coffee. By cutting that down, I saved over $50 a month! This small change made a big difference.

Frequently Asked Questions

1. Why is a budget important after getting my first job?

A budget helps you understand your finances and can prevent you from overspending. It ensures that you have enough money for essential expenses, savings, and fun. For example, if you know you have $200 for entertainment, you won’t go overboard.

2. How do I start creating a budget?

Begin by listing your income and all your expenses. Use a simple spreadsheet or a budgeting app. Allocate your earnings to different categories like rent, food, and savings. This way, you can see where every dollar goes.

3. What if I have irregular income?

If your income fluctuates, try to budget based on your lowest earning month. This way, you won’t overspend in months when you earn more, and you’ll be prepared for leaner months.

4. Should I include savings in my budget?

Absolutely! Treat savings like a bill. Set aside a certain amount each month to save for emergencies or future goals. Even $20 a month adds up!

5. How often should I review my budget?

It’s a good idea to review your budget every month. Look for areas where you can cut back and adjust your goals as needed. This will keep your budget relevant and effective.

Recap / Final Thoughts

Mastering your money isn’t about restriction—it’s about intention. Start by applying just one or two of these strategies today. Small steps lead to big results. Remember, creating a budget after getting your first job sets you on the path to financial freedom!

Take charge of your finances today! Remember, it’s never too late to start budgeting. You have the power to shape your financial future.

Recommended Next Steps

Now that you know the basics of creating a budget after getting your first job, here are some steps to follow:

- Start tracking all your expenses.

- Create a zero-based budget.

- Automate your savings.

- Set clear financial goals.

For more insights into forex trading, check out Investopedia and NerdWallet.

Expand Your Knowledge

- 📌 Financial Planning Tips & Strategies

- 📌 Budgeting Techniques

- 📌 Debt Management

- 📌 Insurance & Financial Security

- 📌 Loan Managing Solution

- 📌 Outsourcing & Finance

- 📌 Passive Income Ideas

- 📌 Saving and Investing

- 📌 ———————————-

- 📌 Affiliate Marketing

- 📌 Blogging

Start Trading Today

Ready to take your forex trading to the next level? Open an account with Exness, one of the most trusted platforms in the industry. 👉 Sign Up Now and trade with confidence!

My recommended broker stands out with ultra-low spreads for beginners, instant withdrawals, and zero spread accounts for pro traders.

Trusted since 2008, lightning-fast execution, no hidden fees, and a secure, transparent trading environment—giving you the edge you need to succeed. 🚀

Watch this helpful video to better understand creating a budget after getting your first job:

Note: The video above is embedded from YouTube and is the property of its original creator. We do not own or take responsibility for the content or opinions expressed in the video.

Starting your first job is an exciting milestone, but it also comes with a host of financial responsibilities that can feel overwhelming. To navigate this new phase, it’s crucial to establish a solid financial foundation. One of the first steps you should take is setting up your 401(k) account. Many young professionals overlook this opportunity and delay setting it up for months or even years. By contributing early, you not only begin saving for retirement, but you may also benefit from employer matching contributions, which is essentially free money. Additionally, contributions to a 401(k) reduce your taxable income, giving you a better handle on your annual tax bill. To maximize your financial health, creating a budget is essential. This involves understanding your expenses, including student loans, rent, food, and discretionary spending. While it may be uncomfortable to face these numbers, having a clear picture of your finances empowers you to make informed decisions and helps you manage your money more effectively.

Another important aspect of financial management involves understanding and building credit. Many young adults are unaware of how to establish a good credit history, which is vital for future financial endeavors such as renting an apartment or securing loans. One effective way to start building credit is through a secured credit card, where you deposit money that serves as collateral. This is generally easier to obtain without a credit history. However, it’s important to use credit wisely—think of a credit card as a tool rather than a means to overspend. When renting your first apartment, consider sharing costs with roommates to alleviate financial pressure. Be mindful of additional expenses, such as broker fees and utility bills, and consider getting a co-signer if needed. Lastly, while saving may seem daunting, especially when balancing various expenses, aim to set aside any bonuses you receive into a savings account, treating it as extra income that shouldn’t be spent. Establishing these habits early on can lead to long-term financial stability and peace of mind.

For anyone grappling with debt, it’s essential to explore different repayment strategies. Understanding the nuances between the debt snowball and avalanche methods can significantly impact your financial journey. The debt snowball method focuses on paying off smaller debts first, providing quick wins and motivation, while the avalanche method prioritizes higher interest debts, which can save you money in the long run. Each approach has its benefits depending on your situation and financial goals, and choosing the right method can pave the way toward financial freedom. For more insights on this topic, check out our post on understanding debt snowball vs avalanche methods.